After coasting last month during the chaos (no trades in April), we have a tiny hint of clarity, so it’s time to make a few adjustments…

Volatility Back to “Normal”

Volatility is back down to (roughly) where it was on January 1st, 2025. For those of us who like “boring”, this is a step in the right direction.

The Market: Still Not in Charge

Last month I commented that the President is driving the short term direction of the market, rather than the usual drivers….earnings, inflation, unemployment, interest rates.

No change there, but the President’s behavior (raising then lowering tariffs, pausing tariffs) indicates that the “Trump Put” remains, though it's not as reliable as during his first term. In other words, the market believes that there’s a limit to how far the President is willing to stress the economy.

We still don’t have clarity on the tariff policy, but the consensus has gone from “no clue what will happen” to “probably 10% to 30% on China, and 10% on all other countries”.

I think risk remains higher than the VIX would indicate, as effects of price hikes and supply chain disruption won’t be visible until June/July. However, the outlook has improved since early April.

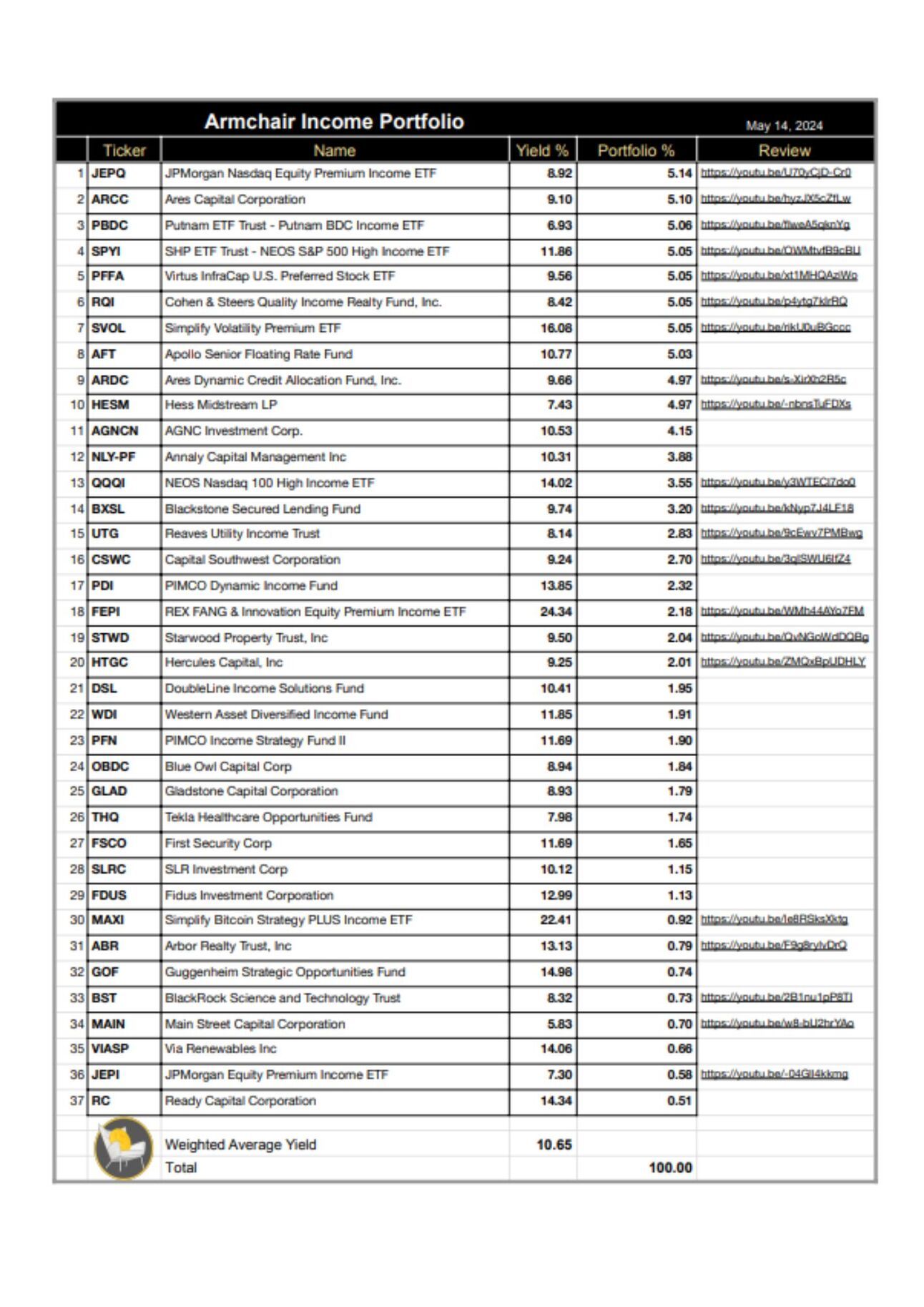

In that context, I’m edging back into equities by adding back some JEPQ. However, I’m mostly focused on increased diversification via gold, international stocks, and Bitcoin, as outlined below.

Trades

Sold DX-C (2.52% Allocation)

This preferred stock recently switched from fixed to floating rate, which means the yield will increase from 6.7% to approx 10% (assuming no change to the Fed Funds rate) on July 15th. I still like this stock as much as when I reviewed it here in this March 2025 episode.

So why sell it?

It’s a low volatility place holder. Over the past 6 months it has been a stable place to park some cash.

DX.C has been a Steady Eddie.

Going forward, if I would happily buy it back again. The positives are: #1/ Stable price #2/ Steady 6.7% yield, soon to be 10ish %. The negatives are: #1/ Concentration in 1 mortgage company #2 Priced above $25.

The intent of the purchases below are to diversify risk beyond US equities and credit (this one is hybrid of both, but behaves more like credit).

DX.C is callable at $25 so any price above that number represents “call risk”. In other words, if the shares were redeemed or “called” at $25, shareholders would only receive $25 plus any accrued and unpaid dividends. For this reason, I’m selling this preferred rather than, say EICC, which is priced (below $25) at $24.93.

There’s nothing wrong with this preferred stock, and just because I want more diversification, doesn’t mean other investors have the same wants/needs. I also considered trimming all preferreds slightly rather than selling 2, but my portfolio is already long at 35 holdings, and I’m trying to keep it on one page!

Sold NLY-F (3.34% Allocation)

This one is paying 9.3% and the reasoning for selling is the same as described above for DX-C. I still like both of these preferreds, and may purchase them again in the future.

Bought IDVO (1.85% Allocation)

Investing outside the US? Plenty of options for growth and value investors, but slim pickings for income investors. IDVO is the only one I’ve found that works for me.

The 5.73% yield is lower than I’d normally consider. However, I’m open to yields below 8% if 1/ I get something in return and 2/ My portfolio continues to yield more than 8%. Adding some high yielding BTCI as described below, more than makes up for the low yield from this fund.

Aside from diversification beyond the US, IDVO offers a history of distribution growth….a 27% increase since its 2022 inception.

Most high yield investments don’t offer much distribution growth. Also, total return since inception is similar to the S&P 500. I plan to create an episode about IDVO in the future.

If you don’t want to wait for that, here’s an analysis of IDVO by Cain Lee who covers several income funds on Seeking Alpha.

Bought: IGLD (1% Allocation)

After searching for an income fund based on Gold, IGLD is the only one I could find that offers a history of consistent income (approx 7% yield). It sells covered calls on a synthetic gold position, based on the almighty GLD fund ($100b assets under management).

Gold is hot right now, and there’s a risk that it will peak soon. However, this is a move toward diversification as gold often behaves differently to other asset classes. For example, Gold, the S&P 500, and Bitcoin have recently moved independently.

I don’t know what the future price trend of gold will be, but the price is very high right now, so I would like to expand this position on dips. I recently reviewed IGLD in detail in this episode.

BTCI: Increased Allocation from 1.12% to 2.11%

Of the 2 Bitcoin income funds I hold, I prefer the more consistent income offered by BTCI. The yield typically ranges from 25-30%. Annualizing the most recent $1.2591 distribution equates to a yield of 25%. Thus, a small allocation moves the needle for portfolio income.

With a yield that high, comes the high volatility that Bitcoin is known for. A 50-80% correction is always a potential risk. I’m increasing the allocation because Bitcoin performed well during the tariff chaos as explained in this recent episode about Bitcoin Income ETF’s. I consider it diversification away from equities, credit, interest rates, tariffs, and the US dollar.

Going forward, I’m open to increasing the combined allocation to BTCI and BITO up to a maximum of 5%. However, Bitcoin is currently at an all time high, so I’d prefer to wait for dips before reaching a full allocation.

JEPQ: Increased Allocation from 2.53% to 4.53%

Covered call funds can experience a short term spike in income, because they receive higher premiums for selling calls when volatility is elevated. JEPQ is a good example as shown below.

JEPQ distributions had a nice pop recently

Now that volatility has returned to “normal”, so too will the distributions. There’s also a risk that if the NASDAQ 100 (and therefore JEPQ) experiences a prolonged correction, then distributions will eventually follow.

As explained above, my outlook for the coming year has improved moderately, hence the slightly higher exposure to equities.

Recent Videos

(Published Since the Last Edition of Armchair Insider)

Armchair Insider Portfolio

(*If you have difficulty opening the portfolio directly from your email, try opening the newsletter in a browser, then opening the portfolio)

Basic Resources

Dividend Tracker: Snowball

Primary Research Tool: Seeking Alpha

How I Use Seeking Alpha to Find Income Stocks/Funds: Video Tutorial

Closed End Fund Database: CEF Connect

Advanced Resources

How to Buy Preferred Shares: 67 Page Guide to Preferred Shares

Preferred Stock Profiles (Rates, Call Dates, etc): Quantum

BDC Weekly Insights Report: Raymond James

Thanks for stopping by…see you in the next issue!

Regards,

Armchair Income

Disclaimer: I’m sharing information about my investments, but I’m not making any recommendations to you to buy or sell anything. Each investor has their own goals, risk tolerance, and timeline, and must make their own investments decisions…then take responsibility for those decisions. I’m not a financial advisor, and I don’t advise anybody regarding their investments. If the information in this newsletter is useful or helpful in any way, then my goal is achieved :) Some of the links provided above may be associated with affiliate programs. If so, use of those links will not incur any additional cost to the user (and will, in many cases, provide a benefit to the user) and may result in a referral commission to this newsletter.